Analysis

The Daily Fix – US retail sales leading us into the FOMC meeting

With some prominent opinion writers publicly stating they are in the 50bp cut camp, US swaps went on a violent ride on the day – where at one stage we saw 42bp of implied cuts for Wednesday's Fed meeting, before retracing some of these expectations and flat-lining through US trade with swaps traders feeling 37/38bp of cuts felt fair. This pricing was one of many factors that held back the USD, where on the day, we saw good net buying flow in GBPUSD, and AUDUSD, with USDNOK also finding sellers.

Trade was impacted yesterday by holidays in China and Japan, so with Japan back online today we’ll see how Japanese traders look to trade the JPY, given we see increased vol in USDJPY, with the spot rate back up at 140.73, having been as low as 139.58. USDCAD has been whippy intraday but looks towards the CAD CPI (22:30 AEST) print, where economists expect CAD headline CPI to pullback to a 2.1% y/y pace, and core CPI at 2.2% (from 2.4%) – with CAD swaps pricing 37bp of implied cuts for the next BoC meeting on 23 October, the CPI print could have implications on the markets other 25bp vs 50bp rate cut debate.

The highlight and key event risk in the session ahead will be US retail sales, where economists see a risk of a 20bp m/m decline in sales in August, although this negative dynamic may be offset by an expected 30bp m/m increase in the ‘control group’ element – that is, the more targeted elements of sales that feed more intently into the US GDP calculation. Weaker retail numbers could naturally weigh on risk, and may further impact US swaps pricing, pushing the implied level of cuts towards 40bp – that said, while semantics are at play, one must feel strongly that the respective voting Fed members have already made up their minds on this week’s rate decision, and as such the influence on cross-assert volatility from the retail sales report may be reduced.

The four US equity indices I track – the S&P500, NAS0100, DJ30, and Russell 2k - closed out with mixed fortunes in the respective close-to-close percentage changes, with the Dow (+0.6%) the outperformer, while the NAS100 (-0.5%) was dragged lower by Apple (-2.8*%), Nvidia (-2%) and Tesla (-1.5%). The bulls will try and claim the session though, with both the S&P500 and NAS100 cash index trading weaker in early trade before the buyers wrestled control and drove the respective indices higher consistently throughout trade. The S&P500 ultimately closed near session highs, with 75% of S&P500 companies higher on the day, led by financials, energy, and materials. So, while growth may have taken a backseat, the value areas of the market stood up and found the love.

Energy markets have seen enough movement and intraday trend to attract the day traders, with WTI crude gaining 2.7% pushing into $70.50, and breaking above Friday’s highs – a reason for shorts to pare back on an extensive short position. Copper and SGX iron ore futures have also gained and supported the rally in S&P500 materials equity names. Gold traded a tight but messy tape, setting a session range of $2589 to $2575, with the bulls still feeling confident that pullbacks, that may eventuate from this week’s FOMC meeting, should be relatively shallow and potentially create an opportunity for would-be buyers to get set at better levels.

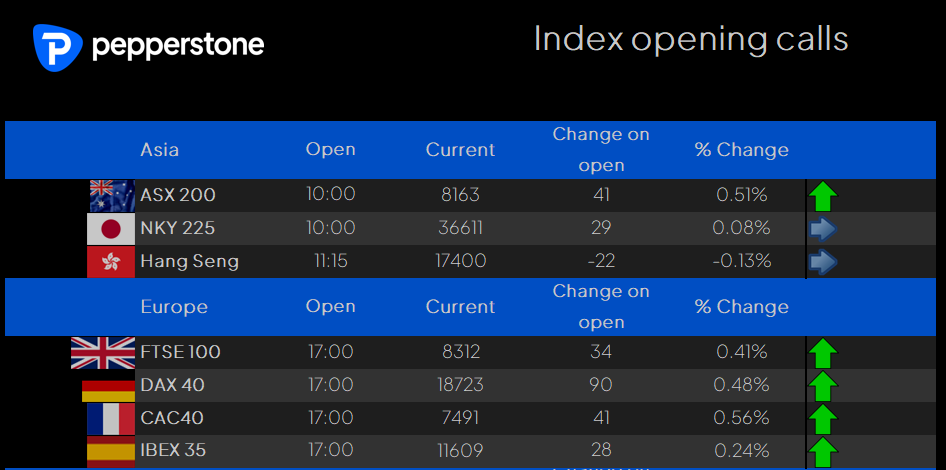

Turning to Asia – When financials, materials and energy were the best-performing sectors in the S&P500 the read-through for the ASX200 is typically a positive affair. I note then that our current opening call for the ASX200 suggests we are set for new all-time highs to come into play on the open. We can already see Aus SPI futures breaking to new ATHs - so while the Aussie equity and futures market may be a lower beta index, it is working like a dream at present – even more so on a total return basis – and with Aussie 10yr yields at 3.81% and the lowest yield since June 2023 – those approaching retirement would be feeling very comfortable indeed today.

China remains closed but Japan is back online, where the NKY225 plays catch up, albeit our call suggests an uneventful re-open, but as many look to further position portfolios ahead of the Fed meeting, the possibility of more lively conditions is there.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.